English

English

Published: March 25, 2026

Published: March 25, 2026

Editor: Ruoxi

Editor: RuoxiWhat are the conditions for VAT refund?

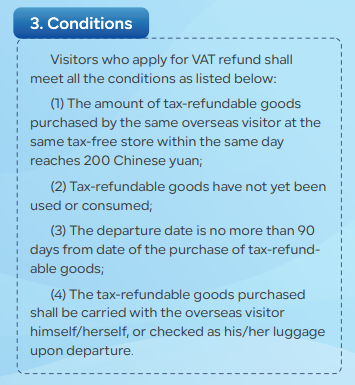

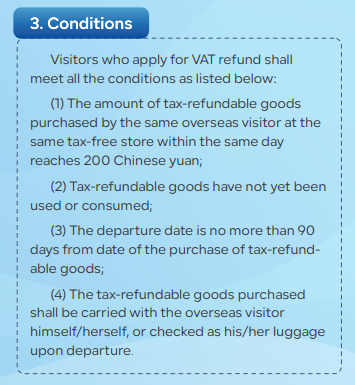

Visitors who apply for VAT refund shall meet all the conditions as listed below:

(1) The amount of tax-refundable goods purchased by the same overseas visitor at the same tax-free store within the same day reaches 200 yuan RMB;

(2) Tax-refundable goods have not yet been used or consumed;

(3) The departure date is no more than 90 days from date of the purchase of tax-refund-able goods;

(4) The tax-refundable goods purchased shall be carried with the overseas visitor himself/herself, or checked as his/her luggage upon departure.

How to calculate the amount of tax refund?

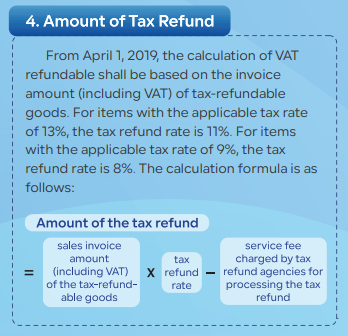

As of April 1, 2019, the calculation of VAT refundable shall be based on the invoice amount (including VAT) of tax-refundable goods. For items with the applicable tax rate of 13%, the tax refund rate is 11%. For items with the applicable tax rate of 9%, the tax refund rate is 8%.

The calculation formula is as follows:

Amount of the tax refund=sales invoice amount (including VAT of the tax-refundable goods) × tax refund rate -service fee charged by tax refund agencies for processing the tax refund.

What items are eligible for VAT refund?

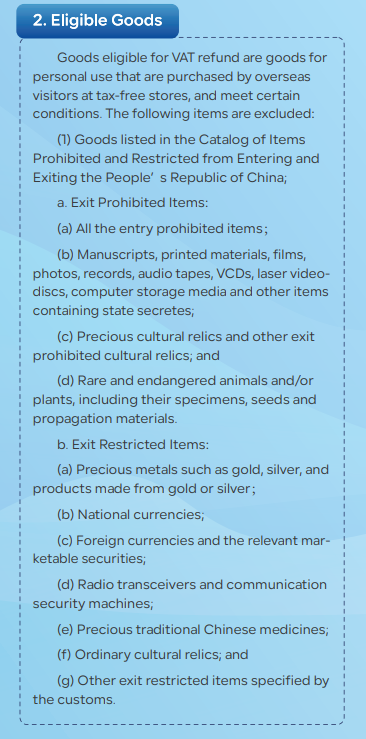

Goods eligible for VAT refund are goods for personal use that are purchased by overseas visitors at tax-free stores, and meet certain conditions. The following items are excluded:

(1)Goods listed on the Catalog of Items Prohibited and Restricted from Entering and Exiting the People's Republic of China;

a.Exit Prohibited Items:

(a)All the entry prohibited items;

(b)Manuscripts, printed materials, films, photos, records, audiotapes, VCDs, laser video-discs, computer storage media and other items containing state secretes;

(c)Precious cultural relics and other exit prohibited cultural relics; and

(d)Rare and endangered animals and/or plants, including their specimens, seeds and propagation materials.

b.Exit Restricted Items:

(a)Precious metals such as gold, silver, and products made from gold or silver;

(b)National currencies;

(c)Foreign currencies and the relevant marketable securities;

(d)Radio transceivers and communication security machines;

(e)Precious traditional Chinese medicines;

(f)Ordinary cultural relics; and

(g)Other exit restricted items specified by the customs.

(2)Items sold at tax-refund shops that are subject to the VAT exemption policy;

(3)Other items stipulated by the Ministry of Finance, the General Administration of Customs, and the State Taxation Administration.

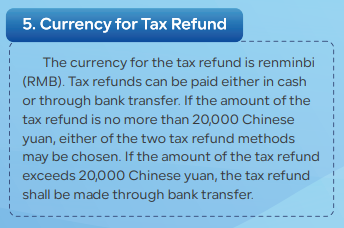

What is the currency used for the tax refund?

The currency for the tax refund is renminbi (RMB). Tax refunds can be paid either in cash or through bank transfer. If the amount of the tax refund is no more than 20,000 Chinese yuan, either of the two tax refund methods may be chosen. If the amount of the tax refund exceeds 20,000 Chinese yuan, the tax refund shall be made through bank transfer.

Currently, which regions in China have implemented the tax refund policy for overseas visitors?

As of present (November 19), 33 regions in China have implemented the tax refund policy for overseas visitors: Beijing, Shanghai, Tianjin, Anhui, Fujian, Sichuan, Xiamen, Liaoning, Qingdao, Shenzhen, Jiangsu, Yunnan, Shaanxi, Guangdong, Heilongjiang, Shandong, Xinjiang, Henan, Ningxia, Hunan, Gansu, Hainan, Chongqing, Hebei, Guangxi, Jiangxi, Zhejiang, Ningbo, Dalian, Hubei, Jilin, Guizhou, and the Inner Mongolia autonomous region.

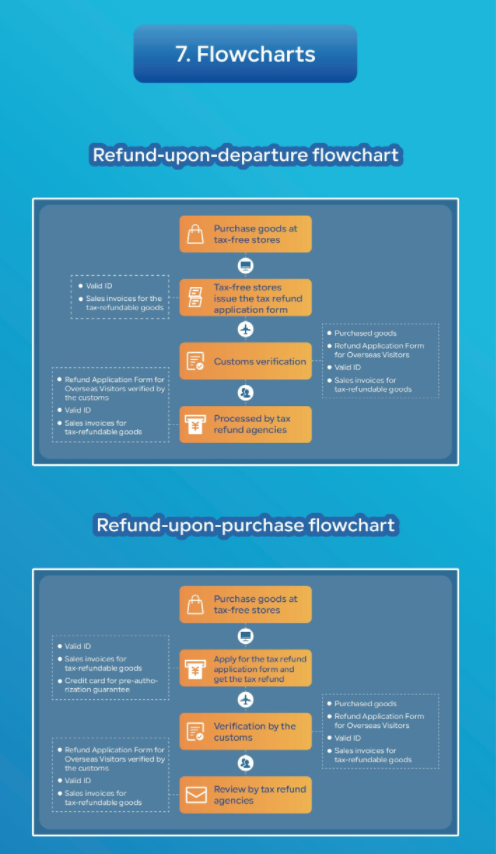

How to apply for the Refund-Upon-Purchase service?

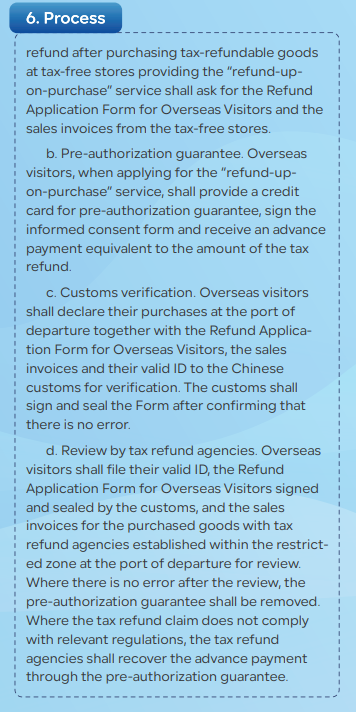

a. Purchasing tax-refundable goods. Overseas visitors who apply for the departure tax refund after purchasing tax-refundable goods at tax-free stores providing the "refund-up-on-purchase" service shall ask for the Refund Application Form for Overseas Visitors and the sales invoices from the tax-free stores.

b. Pre-authorization guarantee. Overseas visitors, when applying for the "refund-up- on-purchase" service, shall provide a credit card for pre-authorization guarantee, sign the informed consent form and receive an advance payment equivalent to the amount of the tax refund.

c. Customs verification. Overseas visitors shall declare their purchases at the port of departure together with the Refund Application Form for Overseas Visitors, the sales invoices and their valid ID to the Chinese customs for verification. The customs shall sign and seal the Form after confirming that there is no error.

d. Review by tax refund agencies. Overseas visitors shall file their valid ID, the Refund Application Form for Overseas Visitors signed and sealed by the customs, and the sales invoices for the purchased goods with tax refund agencies established within the restricted zone at the port of departure for review. Where there is no error after the review, the pre-authorization guarantee shall be removed. Where the tax refund claim does not comply with relevant regulations, the tax refund agencies shall recover the advance payment through the pre-authorization guarantee.

Refund-upon-departure flowchart

Precautions

Items eligible for tax refund must be carried personally by the traveler or checked in as accompanying luggage upon departure. When processing the relevant procedures, customs will verify whether the traveler's valid identification documents match the information of the purchaser stated on the tax refund application form.

During the physical inspection, if the items presented by the traveler correspond to those listed on the application form, customs will confirm and stamp the form. If there is a discrepancy between the quantity of items presented and the quantity listed on the application form, customs will confirm and stamp based on the actual quantity. The traveler may then proceed with the tax refund procedure using the stamped form.

Items submitted for inspection must remain unused or unconsumed. When overseas travelers present these items to customs upon departure, customs will also verify the usage status of the goods.